{kind=link}

Credit cards are something that a user is more likely to come across than investments. I remember someone had questions about them a while back on c/main.

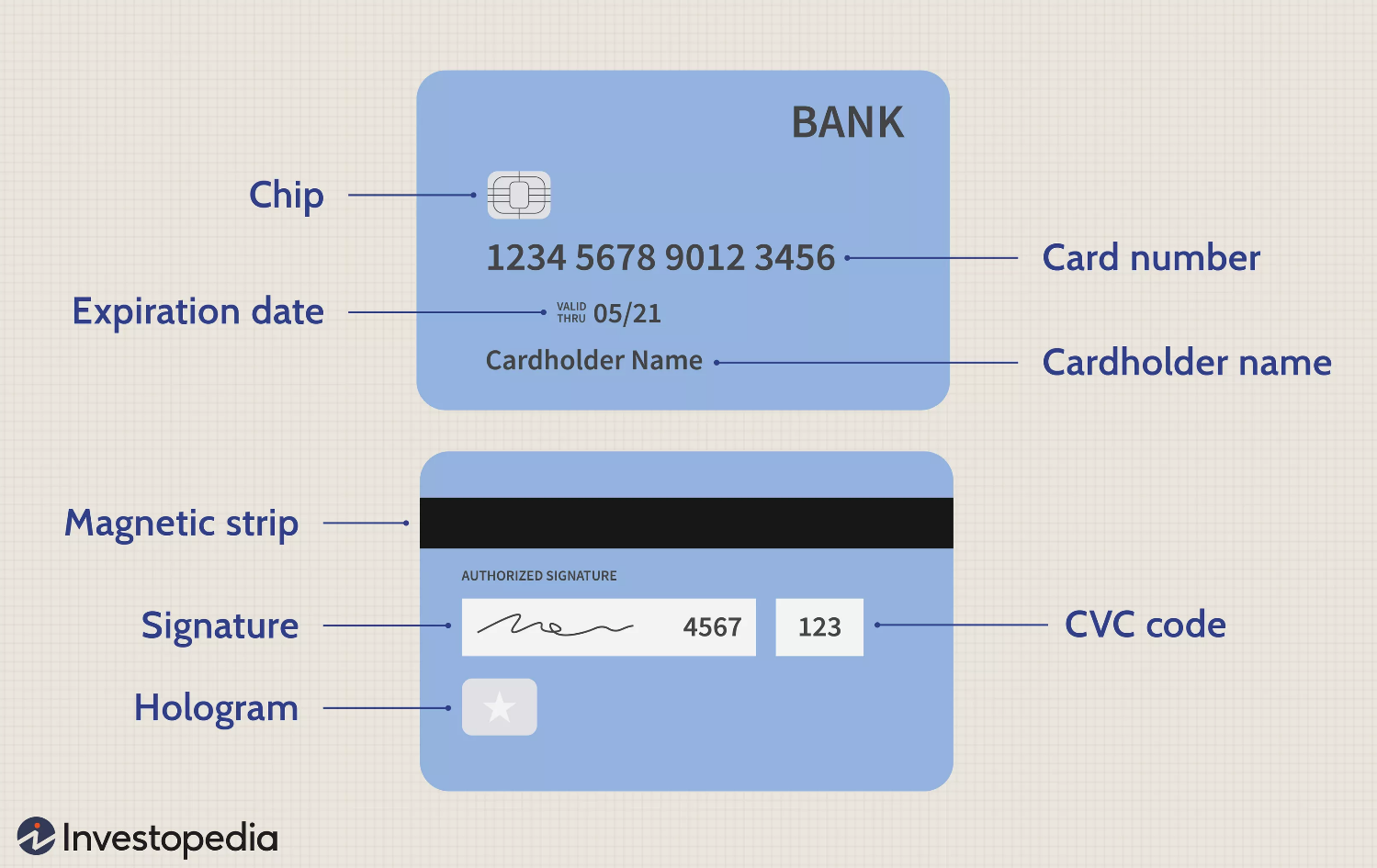

APR - Yearly interest on money borrowed. It varies depending on your existing credit (or lack thereof) as well as what the credit company is offering. Usually when you're just starting out you'll get high APRs. This means when you borrow, there's high interest. That doesn't mean you shouldn't use the cards with high interest, just that you should pay it back quickly and be very careful what you borrow on them. Eventually you may get an offer with 0% APR for a limited time (several months or a year). It's important to note that cards will have variable APR meaning if you're late then the interest rate raises. This is part of why CCs can be bad.

Credit limit - How much you can borrow in total. Borrowing up to this limit can influence your credit score. You don't want to constantly be using a high percentage of your credit limit. CC companies will notice and probably offer to up your limit or send you new cards. This is predatory and you should watch out for it.

Annual Fee - Some cards require you to pay to use them. Not unlike banking fees. Try to avoid these cards if you can. You might have to deal with a few of them while building credit but at some point, but eventually you should get good enough offers that there will be no annual fees.

Credit Score - This isn't only tied to your credit cards, but anything you borrow. Using too much of your credit can cause it to go down. Getting a lot of cards at once can cause it to go down. If you don't use some cards, the CC company will close the account. This could also ding your credit score.

Simple strategy for building credit with CCs: Use them like a debit card but don't spend your cash. Put groceries and gas on a card, pay it off when the bill comes due. Rotate cards as you get more. Don't do any big borrowing unless it's an emergency. It will be tempting to use it on a big purchase, but don't. Once you borrow, if you can't pay it back immediately, the interest starts. And even with the interest free cards, you don't want to collect too much debt and then have an emergency put you behind. By paying off your cards immediately the CC company gets no interest. And if they get no fees either, then you win. You're a deadbeat because you pay off your stuff and they can't weasel any money out of you.

I don't know much about what to do if you have to max out a card for an emergency like dental surgery or car repair. I'd be curious about some strategies there if anyone has them.

Also, Obummer did sign a bill that made it so after 7 years, lenders have to drop the debt. But they will still hassle you the whole time. It's a tiny silver lining because at least it's not debtors prison and they do have to stop calling you eventually.

Also many credit cards have "cash back" or rewards (usually for groceries and gas) so you may as well take advantage of stuff you already need to buy.