Credit cards are something that a user is more likely to come across than investments. I remember someone had questions about them a while back on c/main.

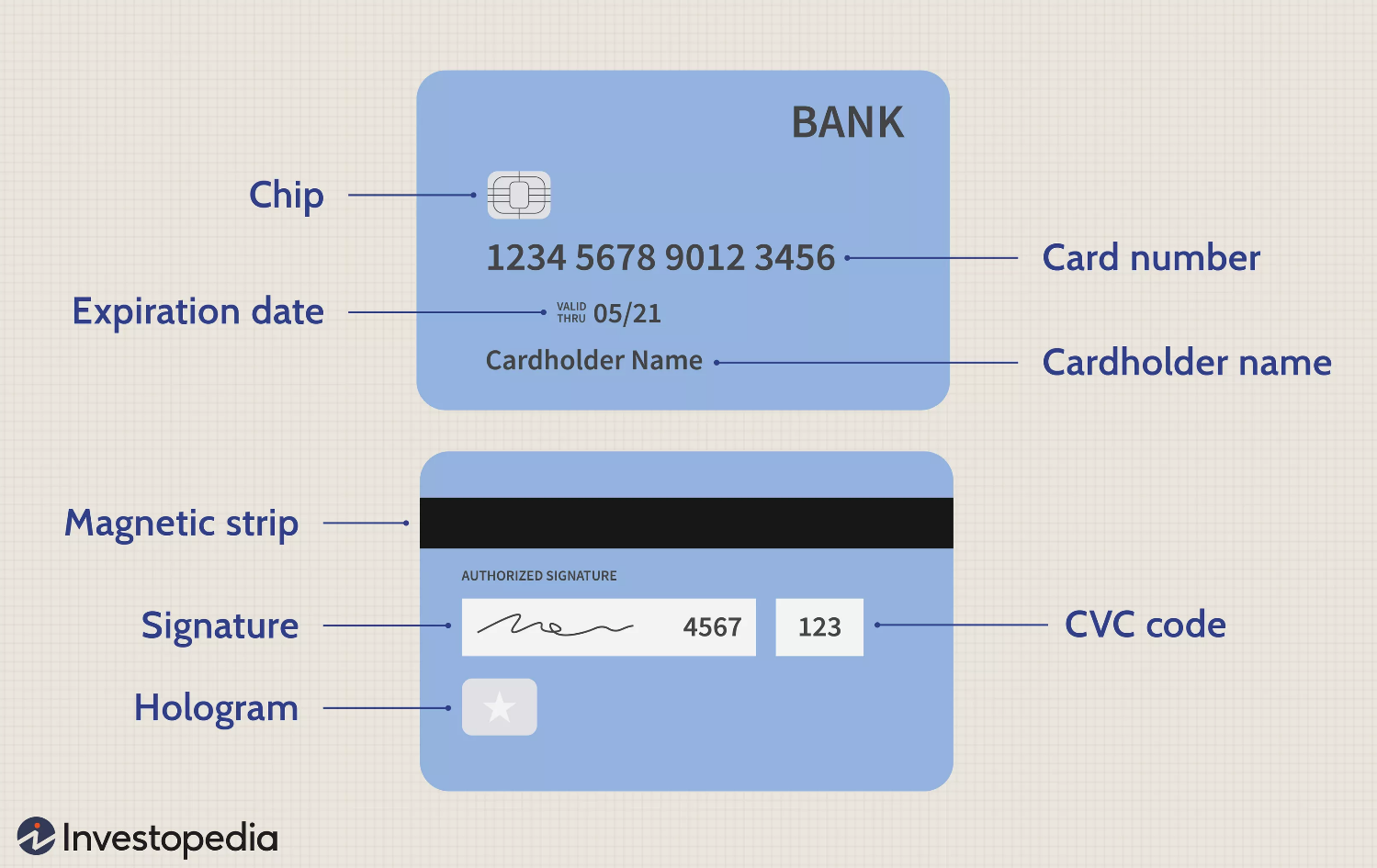

APR - Yearly interest on money borrowed. It varies depending on your existing credit (or lack thereof) as well as what the credit company is offering. Usually when you're just starting out you'll get high APRs. This means when you borrow, there's high interest. That doesn't mean you shouldn't use the cards with high interest, just that you should pay it back quickly and be very careful what you borrow on them. Eventually you may get an offer with 0% APR for a limited time (several months or a year). It's important to note that cards will have variable APR meaning if you're late then the interest rate raises. This is part of why CCs can be bad.

Credit limit - How much you can borrow in total. Borrowing up to this limit can influence your credit score. You don't want to constantly be using a high percentage of your credit limit. CC companies will notice and probably offer to up your limit or send you new cards. This is predatory and you should watch out for it.

Annual Fee - Some cards require you to pay to use them. Not unlike banking fees. Try to avoid these cards if you can. You might have to deal with a few of them while building credit but at some point, but eventually you should get good enough offers that there will be no annual fees.

Credit Score - This isn't only tied to your credit cards, but anything you borrow. Using too much of your credit can cause it to go down. Getting a lot of cards at once can cause it to go down. If you don't use some cards, the CC company will close the account. This could also ding your credit score.

Simple strategy for building credit with CCs: Use them like a debit card but don't spend your cash. Put groceries and gas on a card, pay it off when the bill comes due. Rotate cards as you get more. Don't do any big borrowing unless it's an emergency. It will be tempting to use it on a big purchase, but don't. Once you borrow, if you can't pay it back immediately, the interest starts. And even with the interest free cards, you don't want to collect too much debt and then have an emergency put you behind. By paying off your cards immediately the CC company gets no interest. And if they get no fees either, then you win. You're a deadbeat because you pay off your stuff and they can't weasel any money out of you.

I don't know much about what to do if you have to max out a card for an emergency like dental surgery or car repair. I'd be curious about some strategies there if anyone has them.

Also, Obummer did sign a bill that made it so after 7 years, lenders have to drop the debt. But they will still hassle you the whole time. It's a tiny silver lining because at least it's not debtors prison and they do have to stop calling you eventually.

If you are going to use a credit card regularly, I would highly suggest that you also use some sort of budgeting solution like You Need A Budget so that you don't overspend and end up carrying a balance that you pay interest on.

^^^^^ This

Credit card debt is insanely difficult to be able to pay off.

Also many credit cards have "cash back" or rewards (usually for groceries and gas) so you may as well take advantage of stuff you already need to buy.

I got a credit card when I got my first “real” job and it worked well enough, until I lost that job and tried to live off a credit card with basically no income. I eventually got it paid off but it was not a pleasant experience.

My technique now is to pay my credit card weekly; i shoot to pay it on pay day that way A) it becomes a habit and I don’t forget, and B) it helps me gauge how much of my income I spend.

Credit cards make banks cash from fees, primarily late fees. Once you’re late on a payment, you’re looking at a highly jacked up interest rate (like 30%), possibly in addition to flat fees (usually $20-$50).

Credit cards are great for having a layer of “insulation” between the world and your bank acct (if someone gets your debit card/checking account info it can be a real nightmare, it’s less likely to be a big deal with a credit card), and you can get some cash back by just spending money like you normally would. And using and paying one boosts your credit score pretty significantly, if it’s below “good”

Not sure what its like in the US but in the UK you can just ask your bank to automatically ensure any credit card debt is paid from your debit account before it's been on for a month so you pay no fees or interest. It's good to have so you can use it for regular spending and get rewards like ultraviolet mentioned. Not sure if that's a thing over there though.

Also if anyone has credit card debt, you might be able to transfer the balance to a new card. Some new cards don't charge interest for the first 12 or 15 months so you can transfer a balance from one card to that one for a fee. Like 3-5%

Here's something regarding credit cards/credit lines that may help some people and that they may not be aware of. In fact, I only became aware of the possibility a few months ago. Disclaimer: it does require a 401k and it helps when your company or organization aids in funding it, even if only a little bit.

It's fairly easy to get low(ish) levels of credit on one card or account, something in the $1k-2k range, but even a few hundred will work just fine. I'm going to use my particular circumstance as an example, but this obviously isn't the only way to do it.

I was able to get approved for $1.9k through paypal credit last summer even with a modest credit score. Paypal credit allows you to defer interest (which is an absurd 24%) for the first 6 months on every purchase over $100 (this is not unique to paypal credit, a lot of credit line have similar 'deals' that will be offered). This of course means that at 6 months + 1day you owe that much interest on the purchase. However, one of the advantages of having a 401k is that you can loan yourself money from it (a maximum of around 1/2 of the total amount) at very low interest rates for up to (I think) 5 years. I'm talking 4-6% which is insanely better than the 24% on my paypal credit and most other credit cards. And here's the kicker: the interest you pay back on your 401k goes right back into your 401k. That's right, you're not paying that interest to the bank, you're paying it back to yourself. Now, you have to be careful because if you lose your job or otherwise lose the 401k you're on the hook for the money borrowed immediately; but, then again, you get to set the terms of how long you want to loan that money to yourself from between 1-5 years.

This is great because it's easy for me to make the minimum payments for the first six months, it's something in the neighborhood of $40. And then, toward the end of six months, I loan myself whatever is left on the paypal balance from my 401k and pay myself back to the tune of $40ish dollars a month, only this time it's at 4% interest instead of 24%. And, like I said, that interest I'm paying goes right back into my account instead of disappearing to the bank.

This might be a bit of a tangent but here's my personal experience with credit card debt:

I worked in retail for a few years while living with my parents and still managed to accumulate credit card debt mostly buying small shit like fast food, Dollar Tree items and mobile gacha games. I thought they helped me cope with daily life. Was it fiscally irresponsible to spend more then I was making? Sure, but I was depressed and alienated. Every time I tried to switch jobs to improve my life it made the debt worse and made me feel worthless. Fuck I even tried selling crafts online, but the costs were so high and it basically made my tax refund vanish every year. Anyways, I eventually lucked out with a temp job that became a longer temp job at $15 an hour and only managed to move out with a new roommate's help. Had to save for months just for my half of the apartment down payment since I had to catch up on rent I owed my parents.

By that point I had accumulated $7k in credit card debt. It took me about 2 years to pay it off. I only finished paying it a few months ago and had to immediately switch that money to saving for a down payment on a used car since my old one was starting to die. This month I finally bought the damn car and despite the new monthly payment my budget has eased up. I don't really know what strategy to give other than if you get lucky like I did and manage to get a higher paying job through a temp agency keep living like you work in retail. Learning how to cook is a life long skill and you can start on easier stuff like grilled cheese and salads (hah sorry I think my brain pulled those examples right out of The Sims). Cooking can save you money and help you get the nutrients your body needs to function normally. And if some other piece of shit fellow temp worker dares to make fun of service workers and makes chud "jokes" like, "If they paid everyone $15 dollars what would be stopping me from leaving this job and working at Mcdonald's? They have it so easy!" hold back the urge to start a fight with them because those shitheads aren't worth losing your job over. Just shoot them the dirtiest look you can and then wait a few days to key their car when they park in a spot away from the cameras in minecraft. Oh shit sorry we were talking about credit card debt, my bad. I also heard about the debt snowball method which involves paying off your debts from smallest to highest without considering the interest rates, but since I only had credit card debt to worry about it didn't apply in my case. I've heard good things about it though.

what are the advantages to having more than one? is it just the varying fees and interest rates?

i've avoided getting a credit card my whole life which sucks, but at least i insulated myself from doing anything dumb when i was younger. it's probably time to jump on the train and start building a credit score. the equifax hack still scares me though.

If you have more than one you'll have more credit. Each one is a separate line of credit. Your first cards will have low limits. You be offered higher limits as your credit builds. Higher limits aren't bad on their own, it's just easy to be tempted to use them. But in an emergency having $5000 instead of just $500 can be a literal life saver. The age of your accounts will also help your score. You don't want to close out cards you don't use. And you need to still use them occasionally because some companies will close the account if you don't use them often enough. And each card will have different benefits. Some will be 0% APR. Some will be no fee. Some will have higher or lower limits, different interest rates, etc. It depends on where you live but some places only accept one kind of card. Some places only take visas instead of MasterCard. I don't think that's very common anymore, but it can happen in rural areas. Having more than one type lets you get around that.

sweet

if i wanted to get one, should i just talk to my credit union and go with what they say/give me? or should i go off and do my own research and apply for one from a big bank

go on Nerdwallet they have good comparisions between different cards. That said your credit union's card is probably just fine.

Definitely. Just use the credit card like a debt card and get some of the cashback. They usually have promotional offers when you open a new card with like $100 - $200 cashback if you spend a certain amount (like $500 within 3 months)

{kind=link}